New Administration New Risk

Move over Meta, the Trump Administration is moving fast and breaking things. April 30th marks the first 100 days of this new presidency, which already has brought a whirlwind of change to our country’s economic and business landscape. These new policies bring uncertainty and risk in the U.S., from tariffs, suggested price controls, and monetary policy adjacent measures like influencing the 10-year treasury yield.

Such measures stymie many of the macro assumptions and realities we are accustomed to. Before the election, TRA published an insight on Donald Trump’s then proposed economic policies, and we are now seeing the market recognize that through Executive fiat, these policies are beginning to create measurable impact.

Much has changed in a brief period and at TRA we are taking an objective look at how these changes impact our industry.

Big Law

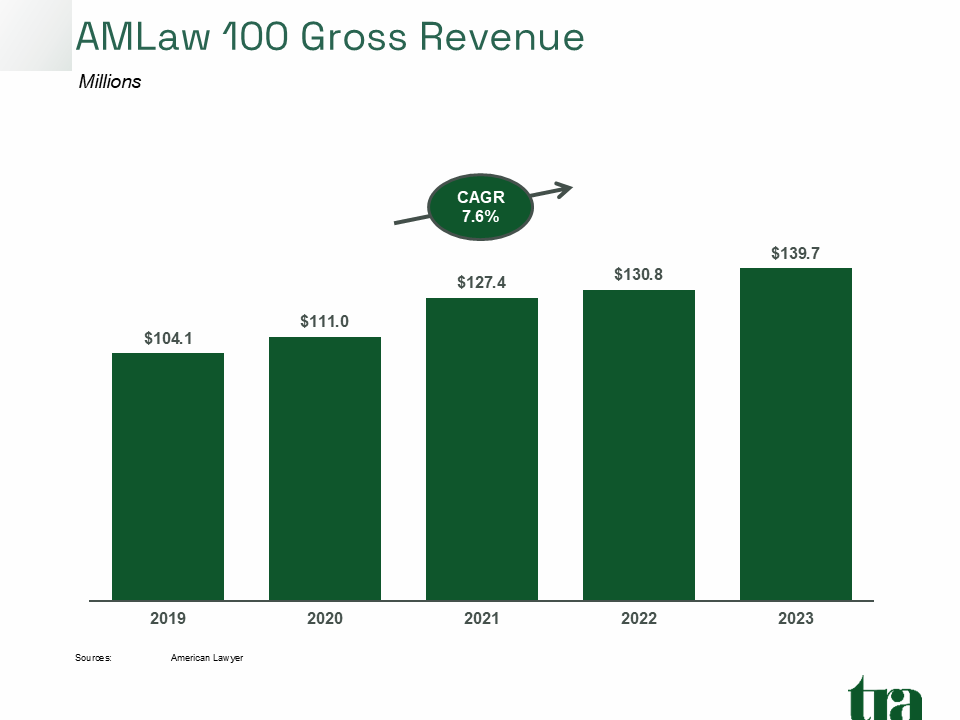

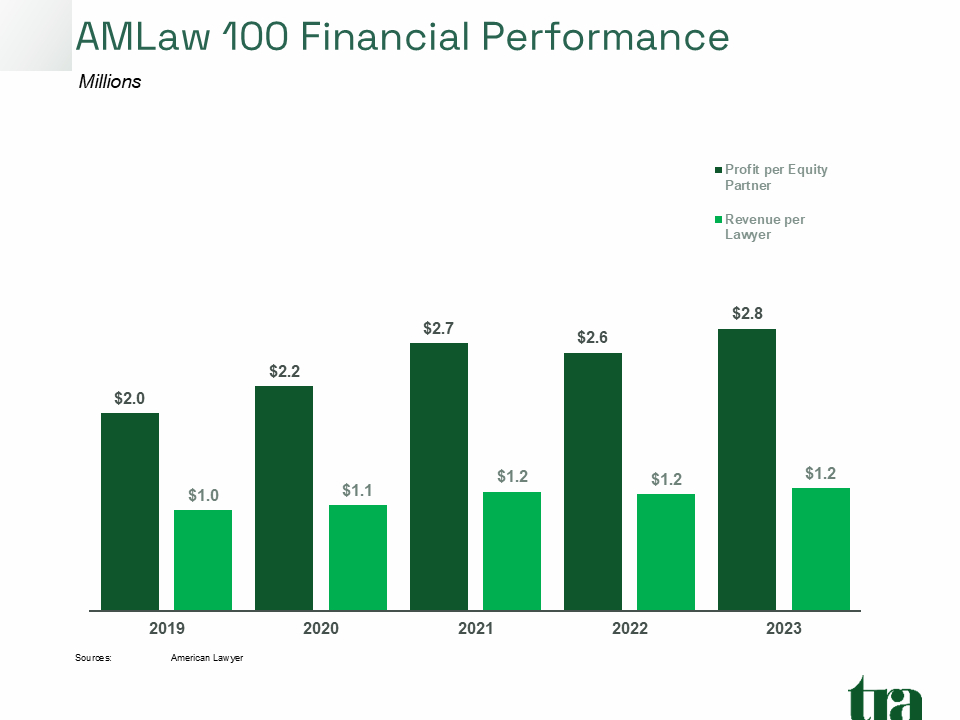

For the past 20 years, with one exception (Dewey & LeBoeuf), Big Law has been a stable commercial tenancy. In fact, profits per equity partner and average revenue per lawyer have been up since 2019, despite the macro uncertainty created by the pandemic. Since Covid’s onset in early 2020, gross fees of the top 100 law firms increased more than 7% compounded annually since 2019.

However, this upward trend is now leveling and the perceived stability of Big Law is being challenged. The Trump Administration has utilized the Justice Department to pursue law firms who prosecuted cases against him personally or his prior administration. High profile law firms of note include Paul, Weiss, Rifkind, Wharton & Garrison LLP (“Paul, Weiss”); Skadden, Arps, Slate, Meagher, & Flom LLP (“Skadden Arps”); Perkins Coie; and WilmerHale, among others. Each law firm has responded differently, with Paul, Weiss’s managing partner negotiating a deal directly with Donald Trump; Skadden Arps preemptively negotiating with the administration; and Perkins Coie and WilmerHale opting to challenge the executive orders that could limit their ability to represent clients in both the public and private

sectors.

Short-and Medium-Term Implications

Working with the administration may ease legal and regulatory pressure now, but it could create reputational risks for a big firm. An attorney or law firm that cannot or will not defend itself may look weak to its clients. Additionally, partners or associates may opt to leave, potentially disrupting the firm’s

efficiency, especially if higher grossing practice areas are impacted. Big Law has been a very lucrative industry since the pandemic’s onset, and attorneys viewing their pipeline of work dry up may be incentivized to defect to greener pastures (or less controversial ones).

The same is true for firms that opt to fight the federal government and the Executive Orders (“EOs”). In the near-term, those firms are at material risk of losing clients with business before the federal government. States, particularly Republican led states, could impose similar restrictions against firms that draw the Trump administration’s ire. There is no easy arithmetic for these law firms to determine the potential economic and fiscal impact of the EOs and their respective approaches.

Long-term Implications

Consolidation was ongoing in 2024, and Fairfax Associates, a law firm consultancy, noted in a report published last fall that more law firm mergers may be coming in 2025. We expect that the uncertainty created by political pressure will slow this trend, at least among firms that fall under the Big Law moniker. Merging law firms are likely to be more considerate of key man risks and ensuring that no partner or attorney has material exposure fighting against the administration or its allies. Additionally, if Big Law capitulates today, it could find a weaker rule of law, which we at TRA assume will be bad for business in ways we cannot currently measure.

Higher Education

Universities, public and private schools, not-for-profits, and for-profits, all benefit from federal government spending, whether it is through federally backed student aid like Title IV, federal government research and development grants, tax incentives, or other federal economic benefits bestowed on colleges and universities. The Department of Government Efficiency (“DOGE”) is downsizing and in some cases eliminating many of these programs. Additionally, schools like Johns Hopkins, Columbia University, Harvard, and others are being targeted directly. In the short term, if these cuts remain, these institutions could shrink head count. Longer-term, they may see reduced need for commercial space, including lab, office, and educational facilities.

In the longer term, these cuts could cool many downstream industries, including pharmaceutical and life science sectors, which are reliant on federal grants that help facilitate early-stage research. Life science and pharmaceutical industries are like the automotive industry, and benefit from agglomeration effects. Life science corridors in the Bay Area, San Diego, and Cambridge, already hurting from weaker capital flows, could see a longer drought if new life science centers arise in countries that are helping to fund groundbreaking research.

Tariffs and the Industrial Sector

The blanket tariffs that the administration has initiated will almost certainly cause prices to increase, growth to slow, and present the economy with a new chapter in the fight against inflation: stagflation. Stagflation occurs when growth is flat, but prices increase. So far, the labor market has remained stable (apart from the DOGE cuts to the public sector and the cascading impact on the private sector), but with labor often being a lagging indicator, the economy could see upticks in unemployment if growth continues softening.

If tariffs remain long-term, prices on items like autos will rise whether they are made in the U.S. or abroad. That could mean the average price of a car increases from just under $50 thousand in 2024 to anywhere from 10% to 15% (assuming the auto makers absorb some of the tariffs themselves). This will impact employment in the auto sector and adjacent businesses, from parts distributors, aftermarket parts providers, and dealerships, which combined employ more than three million people. If this industry cools, it would further soften industrial demand in other sectors too.

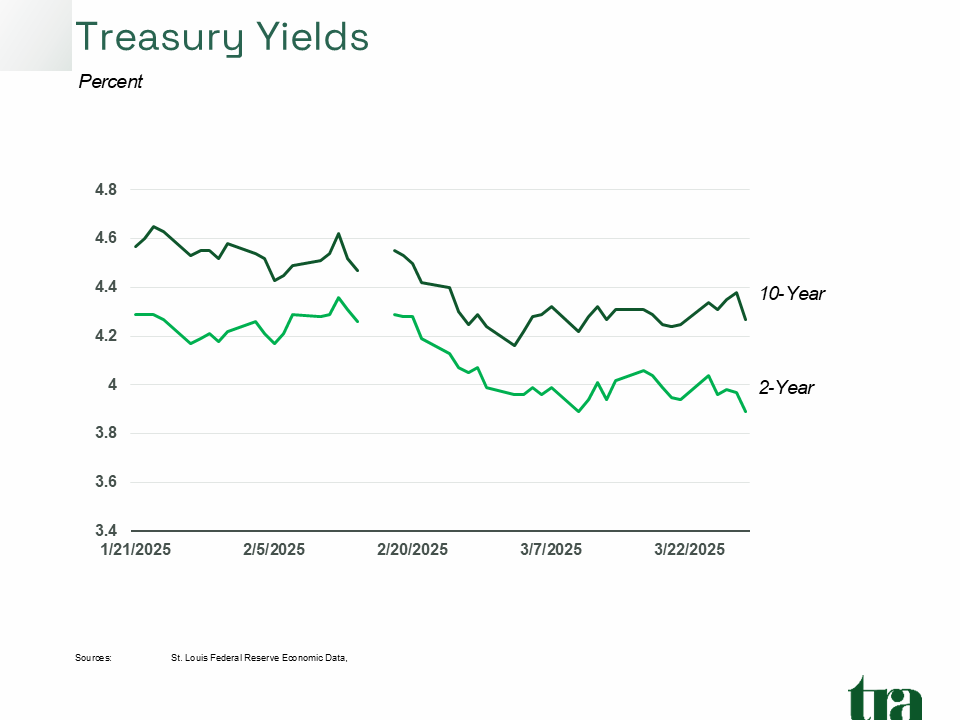

Reading the Treasury Tea Leaves

The Trump administration has put reduction of the 10-year treasury yield as a pillar of its economic agenda. While the Executive Branch cannot directly control 10-year yields, it can, through EOs and tacit support in Congress, control government spending, a material component of the U.S. economy and a key driver of downstream economic growth.

In the early days of the new Administration, the 10-year and 2-year Treasury yields both fell, owing largely to the anticipation of economic activity. After a low in early March, those yields crept back up, primarily on the dual impact of expected weaker GDP growth and the resurgence of inflation stemming

from the administration’s varied and changing tariff strategy. Then, at the end of March, yields began falling sharply again, as the implications of new tariffs across a broad swath of countries and industries arrive in April. Lowering yields on 10-years could result in a weaker dollar and improve U.S. global

competitiveness, but that’s a long-term goal as industries and supply chains reposition themselves for the new economic normal. Assuming growth continues to slow, it is likely that yields will continue falling, all else being equal.

Conclusions

There is much to digest in the economy today and the impact on commercial real estate. If the Administration is successful in its goals to lower the 10-year yield, implement tariffs, and bring some pain to the U.S. economy, rates are likely to continue falling. That would be helpful for commercial real

estate owners that need to refinance mortgages that are rolling in 2025 or 2026. On the other hand, demand for space is likely to decrease across a range of industries due to other secular factors, and it behooves commercial owners to remain thoughtful about tenancy risks related to refinancing or meeting debt service coverage in the coming years. We will continue to monitor the fluid changes as they related to the economic and political landscape, and impact our industry.